Smart Cities: technology trends (Part 3)

Recently I’ve been asked to write a technology trends paper for the IEEE looking at the main technology trends affecting Smart Cities. This is a broad topic, covering a lot of ground and I’ve been forced to pick a subset of technology trends that are affecting the evolution of smart cities. I’ve broken the topic into manageable sections – each a single blog post – as follows:

- PART 1

- Smart cities: background and technology ecosystem

- Key technology areas #1

- Networking,

- Cyber-physical systems and the IoT,

- Cloud and Edge computing

- PART 2

- Key technology areas #2

- Big Data,

- Open Data,

- Citizen Engagement

- Smart City Standards

- Key technology areas #2

- PART 3 (This post)

- Smart Cities: Impact of technology trends

- Business issues

- Recommendations

- Smart Cities: Impact of technology trends

Smart Cities: An overview of the technology trends driving Smart Cities (Part 3)

Business aspects

Although this trend paper focuses on technological trends, as outlined in the introduction, Smart Cities are complex ecosystems that cut across technological, social, organizational and business domains. Understanding the role-out of technologies and their relative importance in the ecosystem requires an understanding of the business drivers that affect their deployment and uptake and an overview of the Smart City marketplace.

Increased urbanization, the development and growth of newer cities, along with the natural renewal of infrastructure in established cities, means that the Smart City marketplace is both large and growing. While the scope and size of the market is difficult to accurately quantify, and estimates vary, all place the size of the market in the $300-700 billion range. For example, a market scoping [1] by the UK’s Department of Trade and Industry, suggests “We estimate the global market for smart city solutions and the additional services required to deploy them to be $408 billion by 2020. Breaking this down by vertical, in transport for example, Pike Research estimates a global market for smart transport solutions based on digital infrastructure to be $4.5 billion by 2018. These solutions are enabling solutions for a wider market of $100 billion by 2018 which includes the physical and digital infrastructure for parking management and guidance, smart ticketing and traffic management. Also included in this $100 billion are the traditional and new services such as heavy engineering, road design and big data analytics which are required as a result of investment in digital smart transport solutions. “

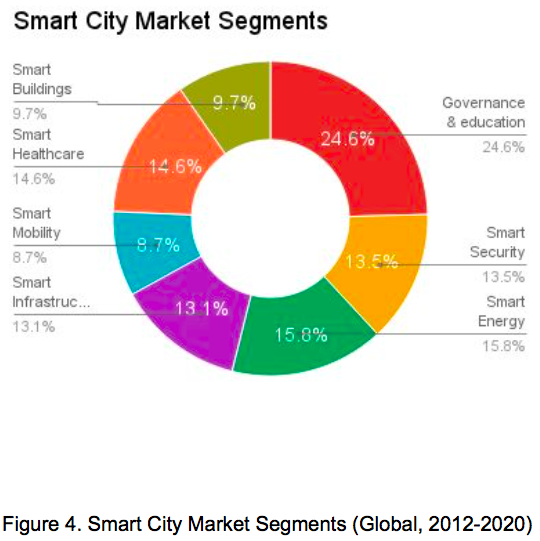

Similarly a report by Frost & Sullivan[2] breaks down the total spend into market segments, identifying Governance & Education, Healthcare and Energy as three of the largest business opportunities.

Trends and recommendations

This report has highlighted a number of technologies whose evolution and deployment is contributing to the growth of Smart Cities. Some high level observations:

- Focus on point solutions: While many major cities are aware of, and to some extent pursuing smart city strategies, it is clear that at the moment most Smart City deployments are focused on specific infrastructure needs. For example reducing water loss by upgrading ageing pipe infrastructure, or improving transportation efficiency through monitoring. Companies need to focus on these types of projects and look for incremental ways to connect individual systems (silos) to provide aggregate efficiencies and support new services.

- Instrumentation and actuation from IoT: As sensors/actuators are being replaced in the system, an increasing percentage of city infrastructure is becoming IoT connected. Cities that are recognizing this and putting in place middleware and cloud systems to capture and use this data will see significant advantages over time.

- Value from analytics: Today few cities gather and analyze city data in a comprehensive way. Some lead examples do exist but most cities are still developing these capabilities. Both government and industry need to adopt big data strategies as part of their core framework, building from a cloud centric perspective solutions that incorporate data analytics as core capabilities. The growth of this area is likely to rapidly increase over the next decade with significant investment by cities in analytic capabilities.

- Different regions have different needs. It is clear that the needs of a Smart City in India are different than those in Europe – different regions are grappling with different problems and so will need different solutions. However, the underlying technology trends do not differ and so the problem becomes the most appropriate application of a technology to meet a city’s needs. Companies that are able to adopt a flexible approach to delivering solution will reap benefits.

- Collaboration is critical. Few, if any companies can deliver a full Smart City solution. Therefore companies need to identify their role in the Smart City solution ecosystem and work to develop partnerships that allow them to collectively offer solutions to cities. Major players will be able to use M&A activity to plug capability gaps.

- Citizen engagement and activism are shaping the thinking of cities. Companies that can tap into this, and can show how their approaches and solution benefit from Citizen Engagement will accrue advantage through differentiation. Cities that develop comprehensive citizen engagement strategies will also benefit from citizens that are franchised as well as the collective wisdom of the community.

Resources

IEEE Smart Cities initiative: http://smartcities.ieee.org/

There has been a significant activity by IEEE to promote Smart Cities and to engage cities in using technologies to develop new services. Examples are Core Cities of Guadalajara in México, Trento in Italy, Wuxi in China, Casablanca in Morocco , Kansas City in US.

Additionally this initiative organized the first two international Conferences on Smart Cities successfully implemented in Guadalajara México 2015 and Trento Italy 2016, being planned the third edition for Wuxi China in 2017.

IEEE Industry activity: http://industry.ieee.org

A portal of IEEE resources targeted at industry and practitioners including content on Professional development, standards and emerging technologies and trends.

BSI Smart Cities: http://www.bsigroup.com/en-GB/smart-cities/

A set of standards focused resources from the British Standards Institute that focus on the Smart City domain.

References

- [1] https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/249423/bis-13-1217-smart-city-market-opportunties-uk.pdf

- [2] http://www.egr.msu.edu/~aesc310-web/resources/SmartCities/Smart%20City%20Market%20Report%202.pdf